Planning for a comfortable retirement

Tina is a fit and vibrant 59-year-old who expected retirement to offer a whole new lease of life. She was looking forward to using her increased leisure time to explore Europe while indulging her passion for climbing. However, after going through her finances, she’s now concerned she won’t be able to afford her monthly bills let alone pay for trips abroad.

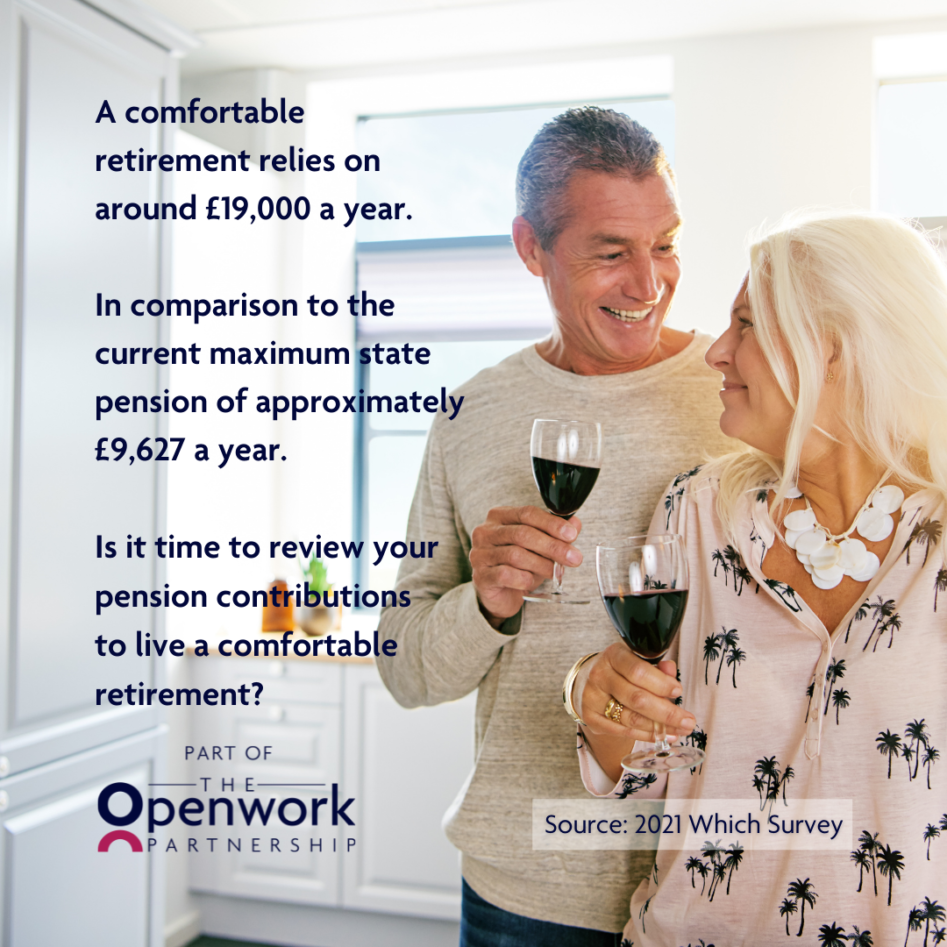

Tina has always managed her day-to-day finances really well, but she never sat down and worked out how much she’d need for a comfortable retirement. A 2021 Which survey found that a retiree in a single-person household spends an average of £19,000 a year and needs £31,000 a year to enjoy luxuries such as long-haul trips and a new car every five years. When you compare this figure with the current maximum state pension of approximately £9,627 a year, it becomes clear relying on that income alone can cause problems.

Why is money going to be so tight for Tina?

There are a number of reasons for this:

Career breaks have affected her state pension entitlement

Tina was a stay-at-home mum throughout most of her 20s and into her mid-30s, when she split up with the father of her children. They were never married so Tina isn’t entitled to any of his pension.

After working full-time for a few years, Tina moved in with another partner and splitting the bills meant she could afford to drop down to part-time hours. She began working full time again when that relationship ended a few years ago and she moved into her own place.

Despite working on and off, Tina hasn’t made anywhere near the 35 years’ worth of National Insurance contributions that guarantee a full state pension. As she’s made more than ten years’ worth of contributions, she’ll get something but nowhere near as much as she expected.

If Tina had checked her state pension forecast regularly, she could have avoided a nasty shock and taken steps to increase her pension pot.

She’s only made minimum contributions to her workplace pensions

Tina’s been enrolled in a couple of workplace pension schemes, but she’s only ever made the minimum contributions required.

There are no fixed rules about how much you should pay into a private pension, but one rule of thumb is to take the age you start saving and divide it by two to give you the percentage of your salary you should put away each year. So, if you start saving at 30, you should pay in 15% of your salary.

It’s worth bearing in mind that the government tops up private pension contributions in the form of tax relief at your highest rate of income tax. Basic rate taxpayers receive tax relief of 20%, while higher rate and additional rate taxpayers can claim back 20% and 25% respectively through their tax returns.

What can you do to boost your pension pot?

There isn’t one simple answer when it comes to saving for your retirement. It’s complicated! So it makes sense to get help from a financial adviser.